Forecasting inflation with AutoML in Amazon SageMaker Autopilot¶

1. Overview¶

Automated Machine Learning (AutoML) frameworks address the expertise- and time-intensive nature of the traditional ML model development workflow. By automating the end-to-end process of building, training and tuning ML models through easy-to-use programmatic interfaces, AutoML solutions make ML accessible to non-specialists and significantly reduce deployment timeframes.

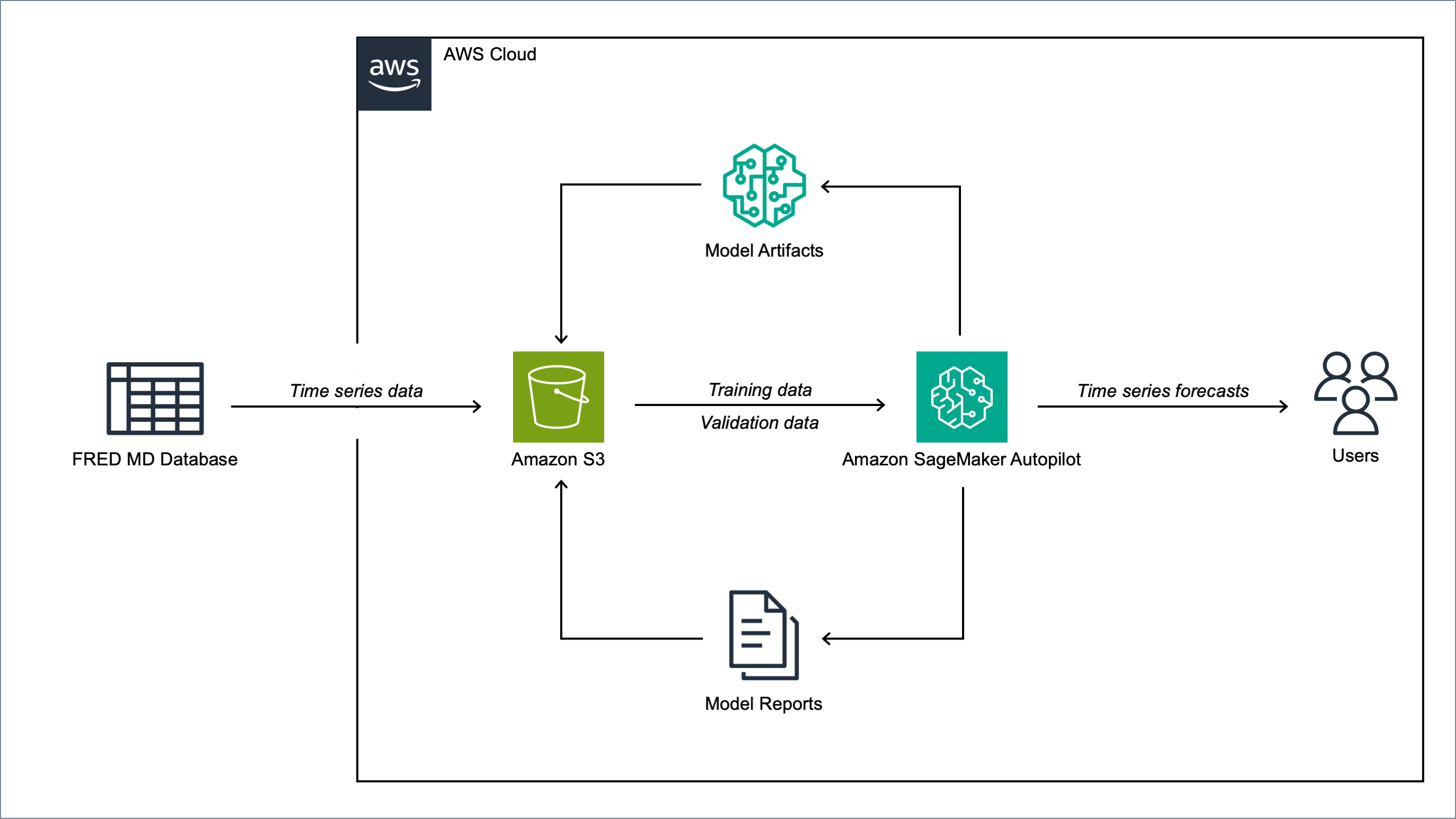

In this post, we demonstrate how to use Amazon SageMaker Autopilot [1], AWS’s AutoML framework, to forecast US inflation using the FRED-MD dataset [2]. FRED-MD is an open-source dataset maintained by the Federal Reserve Bank of St. Louis including over 100 monthly time series of US macroeconomic indicators (see the Appendix for the full list). FRED-MD is widely used in economic research, and has become a standard benchmark for evaluating machine learning models for US inflation forecasting (see, for instance, [3], [4], [5]).

In this demonstration, we use AutoML to forecast the month-on-month (MoM) US CPI inflation. On each month, the model predicts the following month’s percentage change in the US Consumer Price Index (CPI) using the current month’s FRED-MD indicators as inputs. We first run an AutoML job on FRED-MD data from January 1960 to December 2023 to select the best ML pipeline. We then use this ML pipeline in an Amazon SageMaker batch transform job to generate one-month-ahead forecasts from January 2024 to December 2024.

1.1 Amazon SageMaker Autopilot¶

Autopilot is a fully managed AutoML solution designed to automate the end-to-end ML pipeline while maintaining transparency and flexibility. Unlike traditional black-box AutoML systems, Autopilot provides a white-box approach, allowing users to inspect and modify the generated ML pipelines to incorporate domain expertise when necessary [1].

Given a tabular dataset and a specified target column, Autopilot generates a set of candidate ML pipelines optimized for the given dataset’s characteristics and the specific problem type. Each candidate pipeline implements the end-to-end process of data preparation, feature selection and algorithm training. Autopilot then evaluates the candidate pipelines to produce a leaderboard and select the best-performing pipeline.

As part of this process, Autopilot automatically generates a set of data analysis and model insights reports in various formats, along with Jupyter notebooks that allow users to examine and refine the pipelines without reverting to a fully manual approach. Autopilot’s full integration with the broader SageMaker platform allows users to quickly deploy the final selected pipeline in production.

1.2 FRED-MD dataset¶

FRED-MD is a publicly available dataset of U.S. macroeconomic indicators maintained by the Federal Reserve Bank of St. Louis. The FRED-MD dataset was introduced to provide a common benchmark for comparing model performance and to facilitate the reproducibility of research results [2].

The FRED-MD dataset is updated on a monthly basis, with each monthly release referred to as vintage. The vintages are published on the FRED-MD website in CSV format. Each vintage includes monthly data from January 1959 up to the month prior to the release. For instance, the January 2024 vintage includes the data from January 1959 to December 2023. Different vintages can include different time series, as indicators are occasionally added and removed from the dataset.

The FRED-MD time series are sourced from the Federal Reserve Economic Data (FRED) database, which is St. Louis Fed’s main, publicly accessible, economic database. Different retrospective adjustments are applied to the time series sourced from the FRED database, including seasonal adjustments, inflation adjustments and backfilling of missing values. As a result, different vintages can report different values for the same time series on the same date.

The FRED-MD dataset has been used extensively for forecasting US inflation. In [3] it was shown that a random forest model trained on the FRED-MD dataset outperforms several standard inflation forecasting models at different forecasting horizons. [4] applied different dimension reduction techniques to the FRED-MD dataset to forecast US inflation and found that autoencoders provide the best performance. [5] expanded the analysis in [3] to include an LSTM model and found that it did not significantly outperform the random forest model.

2. Solution¶

Note

To be able to run the code provided in this section, you will need to launch an Amazon SageMaker notebook instance. You will also need to download the CSV files with the FRED-MD data from the FRED-MD website and store them in a local folder.

2.1 Set up the environment¶

We start by importing all the dependencies and setting up the Amazon SageMaker environment.

# Import the dependencies

import io

import json

import sagemaker

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.metrics import root_mean_squared_error, mean_absolute_error

# Get the SageMaker session

session = sagemaker.Session()

# Get the SageMaker execution role

role = sagemaker.get_execution_role()

# Get the default S3 bucket

bucket = session.default_bucket()

2.2 Define the auxiliary functions for working with the FRED-MD data¶

Next, we define a set of auxiliary functions for processing the FRED-MD data.

2.2.1

transform_series

The transform_series function transforms each FRED-MD time series according to the assigned transformation code.

The transformation code specifies which transformation the FRED-MD authors suggest applying to each time series in order to make it stationary.

The transformation codes are included in the first row of each CSV file and are defined as follows:

no transformation

first order difference

second order difference

logarithm

first order logarithmic difference

second order logarithmic difference

percentage change

def transform_series(

x,

tcode

):

"""

Transform the time series.

Parameters:

========================================================================================================

x: pandas.Series

Time series.

tcode: int.

Transformation code.

"""

if tcode == 1:

# No transformation

return x

elif tcode == 2:

# First order absolute difference

return x.diff()

elif tcode == 3:

# Second order absolute difference

return x.diff().diff()

elif tcode == 4:

# Logarithm

return np.log(x)

elif tcode == 5:

# First order logarithmic difference

return np.log(x).diff()

elif tcode == 6:

# Second order logarithmic difference

return np.log(x).diff().diff()

elif tcode == 7:

# Percentage change

return x.pct_change()

else:

raise ValueError(f"unknown `tcode` {tcode}")

2.2.2

get_data

The get_data function loads the data for a selected vintage from the

corresponding CSV file and prepares it for the model by transforming and lagging

the time series.

def get_data(

vintage,

series_names,

target_name,

target_tcode,

n_lags,

):

"""

Get the data for a selected vintage.

Parameters:

========================================================================================================

vintage: str.

The vintage of the dataset, in "YYYY-MM" format.

series_names: str.

The time series to be included in the dataset.

target_name: string.

The name of the target time series.

target_tcode: int.

The transformation code of the target time series.

n_lags: int.

The number of autoregressive lags.

"""

# Get the file path

file = f"data/{vintage}.csv"

# Get the time series

data = pd.read_csv(file, skiprows=list(range(1, 11)), index_col=0)

data.index = pd.to_datetime(data.index)

data.columns = [c.upper() for c in data.columns]

data = data.loc[:, series_names]

# Get the transformation codes

tcodes = pd.read_csv(file, nrows=1, index_col=0)

tcodes.columns = [c.upper() for c in tcodes.columns]

# Override the target's transformation code

tcodes[target_name] = target_tcode

# Transform the time series

data = data.apply(lambda x: transform_series(x, tcodes[x.name].item()))

# Add the lags

data = data[[target_name]].join(data.shift(periods=list(range(1, 1 + n_lags)), suffix="_LAG"))

# Drop the missing values resulting from applying the transformations and taking the lags

data = data.dropna()

return data

2.2.3

get_common_series

To ensure consistent data across training, validation, and testing, we define a function that identifies which indicators have complete time series across all consecutive vintages in our analysis period.

def get_common_series(

start_vintage,

end_vintage

):

"""

Get the list of complete time series included in all dataset releases between two vintages.

Parameters:

========================================================================================================

start_vintage: str.

The first vintage, in "YYYY-MM" format.

end_vintage: str.

The last vintage, in "YYYY-MM" format.

"""

# Generate the date range

dates = pd.date_range(

start=f"{start_vintage.split('-')[0]}-{start_vintage.split('-')[1]}-01",

end=f"{end_vintage.split('-')[0]}-{end_vintage.split('-')[1]}-01",

freq="MS"

)

# Create a list for storing the names of the complete time series

series = []

# Loop across the dates

for date in dates:

# Load the data for the considered date

data = pd.read_csv(f"data/{date.year}-{format(date.month, '02d')}.csv", skiprows=list(range(1, 11)), index_col=0)

# Drop the incomplete time series

data = data.loc[:, data.isna().sum() == 0]

# Save the names of the complete time series

series.append([c.upper() for c in data.columns])

# Get the list of complete time series included in the dataset on all dates

series = list(set.intersection(*map(set, series)))

return series

2.2.4

get_real_time_data

To address any potential data leakage, while replicating realistic model usage where the model makes predictions on newly available data, we construct our evaluation set using the last month from each consecutive vintage.

This approach is implemented in the get_real_time_data function, which processes

each vintage using the get_data function and concatenates the final month from

each vintage into a unique Pandas DataFrame.

def get_real_time_data(

start_vintage,

end_vintage,

series_names,

target_name,

target_tcode,

n_lags,

):

"""

Get the real-time data between two vintages.

Parameters:

========================================================================================================

start_vintage: str.

The first vintage, in "YYYY-MM" format.

end_vintage: str.

The last vintage, in "YYYY-MM" format.

series_names: str.

The time series to be included in the dataset.

target_name: string.

The name of the target time series.

target_tcode: int.

The transformation code of the target time series.

n_lags: int.

The number of autoregressive lags.

"""

# Generate the date range

dates = pd.date_range(

start=f"{start_vintage.split('-')[0]}-{start_vintage.split('-')[1]}-01",

end=f"{end_vintage.split('-')[0]}-{end_vintage.split('-')[1]}-01",

freq="MS"

)

# Get the last month of data for each date in the considered range

data = pd.concat([

get_data(

vintage=f"{date.year}-{format(date.month, '02d')}",

series_names=series_names,

target_name=target_name,

target_tcode=target_tcode,

n_lags=n_lags,

).iloc[-1:]

for date in dates

])

return data

2.3 Prepare the FRED-MD data and upload it to S3¶

We now use the functions defined in the previous section for processing the FRED-MD data. We start by defining the target name, the target transformation code and the number of lags used for constructing the features.

Note

We override the suggested transformation for the US CPI,

which is second order logarithmic difference (tcode = 6),

as the resulting time series can’t be interpreted as an inflation rate.

We use percentage changes (tcode = 7) instead, which results in a

MoM inflation rate time series.

# Define the name of the target time series

target_name = "CPIAUCSL"

# Define the transformation code of the target time series

target_tcode = 7

# Define the number of autoregressive lags of each time series

n_lags = 1

After that, we extract the list of complete time series included in all vintages used for the analysis.

# Get the list of complete time series included in all vintages from 2023-01 to 2025-01

series_names = get_common_series(

start_vintage="2023-01",

end_vintage="2025-01",

)

This results in 101 time series, including the target time series.

2.3.1 Training data

For training the candidate models during the AutoML experiment, we use the data from January 1960 to December 2022.

# Prepare the training data

training_data = get_data(

vintage="2023-01",

series_names=series_names,

target_name=target_name,

target_tcode=target_tcode,

n_lags=n_lags,

)

# Upload the training data to S3

training_data_s3_uri = session.upload_string_as_file_body(

body=training_data.to_csv(index=False),

bucket=bucket,

key="data/train.csv"

)

2.3.2 Validation data

For evaluating and ranking the candidate models during the AutoML experiment, we use the data from January 2023 to December 2023, where the data for each month is extracted separately from the corresponding vintage.

Important

If the validation data is not provided, SageMaker Autopilot performs cross-validation on the training data. However, the generated cross-validation splits may not preserve temporal order, resulting in potentially training the model on future data and evaluating it on past data.

# Prepare the validation data

validation_data = get_real_time_data(

start_vintage="2023-02",

end_vintage="2024-01",

series_names=series_names,

target_name=target_name,

target_tcode=target_tcode,

n_lags=n_lags,

)

# Upload the validation data to S3

validation_data_s3_uri = session.upload_string_as_file_body(

body=validation_data.to_csv(index=False),

bucket=bucket,

key="data/valid.csv"

)

2.3.3 Test data

For testing the best candidate model selected by the AutoML experiment, we use the data from January 2024 to December 2024, where again the data for each month is extracted separately from the corresponding vintage. The testing is performed later by performing a batch transform job with the best candidate model to generate the test set predictions.

Important

Make sure to exclude the header and to drop the target column from the test dataset before uploading it to S3, otherwise the batch transform job will fail.

# Prepare the test data

test_data = get_real_time_data(

start_vintage="2024-02",

end_vintage="2025-01",

series_names=series_names,

target_name=target_name,

target_tcode=target_tcode,

n_lags=n_lags,

)

# Upload the test data to S3

test_data_s3_uri = session.upload_string_as_file_body(

body=test_data.drop(labels=[target_name], axis=1).to_csv(index=False, header=False),

bucket=bucket,

key="data/test.csv"

)

2.4 Configure and run the AutoML job¶

We configure the AutoML experiment as a regression task, using mean squared error (MSE) as the validation objective to minimize. The experiment is run in ensembling mode, so the final pipeline combines multiple algorithms rather than returning a single optimized model.

# Define the AutoML job configuration

automl = sagemaker.automl.automlv2.AutoMLV2(

problem_config=sagemaker.automl.automlv2.AutoMLTabularConfig(

target_attribute_name=target_name,

algorithms_config=["randomforest", "extra-trees", "xgboost", "linear-learner", "nn-torch"],

mode="ENSEMBLING",

problem_type="Regression",

),

job_objective={"MetricName": "MSE"},

base_job_name="us-cpi",

output_path=f"s3://{bucket}/output/",

role=role,

sagemaker_session=session,

)

# Run the AutoML job

automl.fit(

inputs=[

sagemaker.automl.automlv2.AutoMLDataChannel(

s3_data_type="S3Prefix",

s3_uri=training_data_s3_uri,

channel_type="training",

compression_type=None,

content_type="text/csv;header=present"

),

sagemaker.automl.automlv2.AutoMLDataChannel(

s3_data_type="S3Prefix",

s3_uri=validation_data_s3_uri,

channel_type="validation",

compression_type=None,

content_type="text/csv;header=present"

),

]

)

After the AutoML job has completed, we can extract the S3 location containing the model artifacts of the final selected pipeline.

# Get the best model

automl.best_candidate()

The AutoML job automatically generates several reports for each candidate pipeline, including a model explainability report with the feature importances and a model quality report with an analysis of the performance on the validation data, which are also saved to S3.

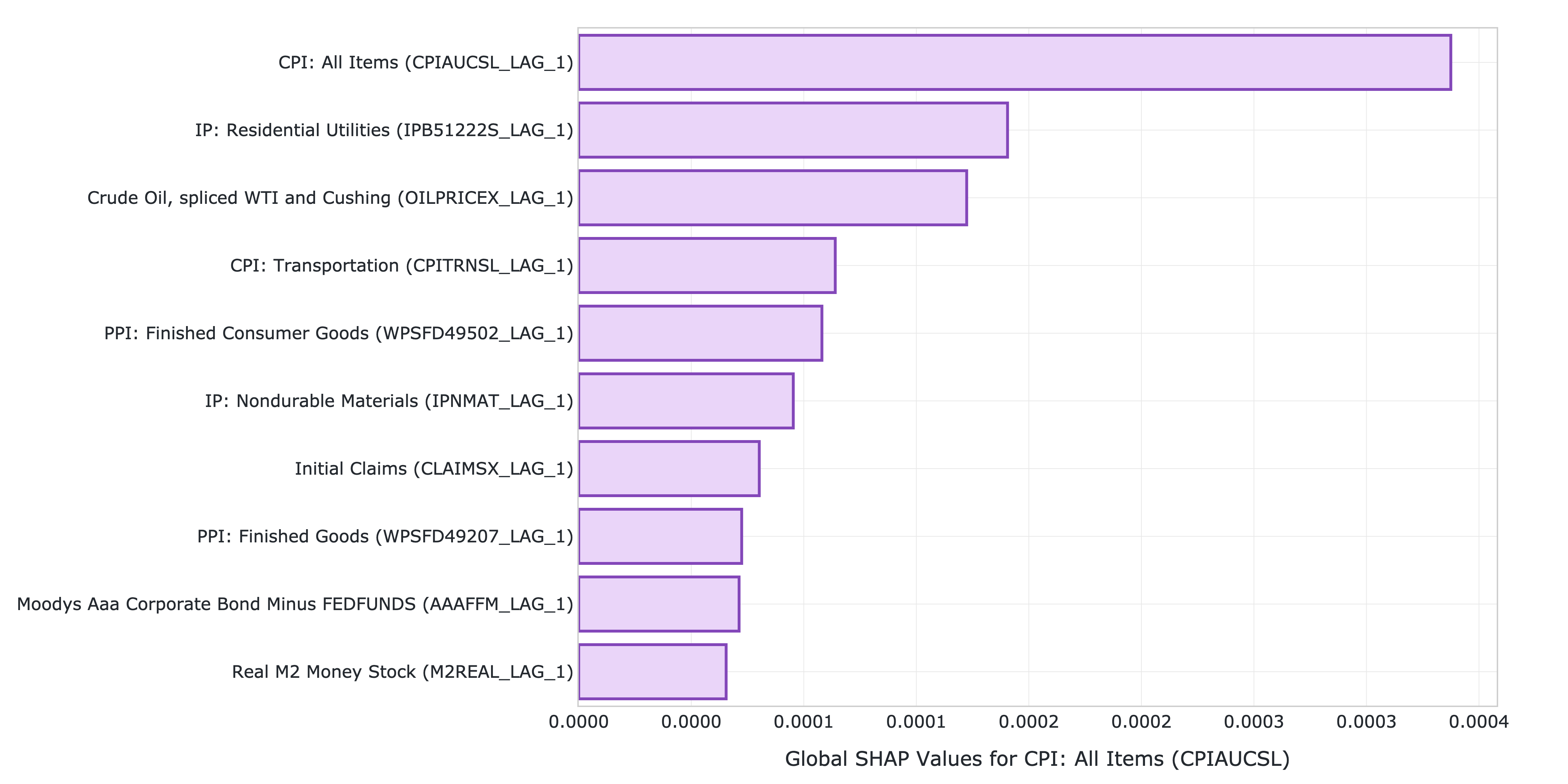

2.4.1 Model explainability report

The model explainability report includes the feature importances calculated using the Kernel SHAP method. The report shows that the previous month’s CPI inflation is the most influential predictor, followed by the industrial production for residential utilities and the crude oil price. Transportation inflation and producer prices for finished consumer goods are also important, while factors such as initial unemployment claims, the AAA corporate bond spread, and real money supply are also relevant, though less significant.

Figure 1: Top 10 features by SHAP value.

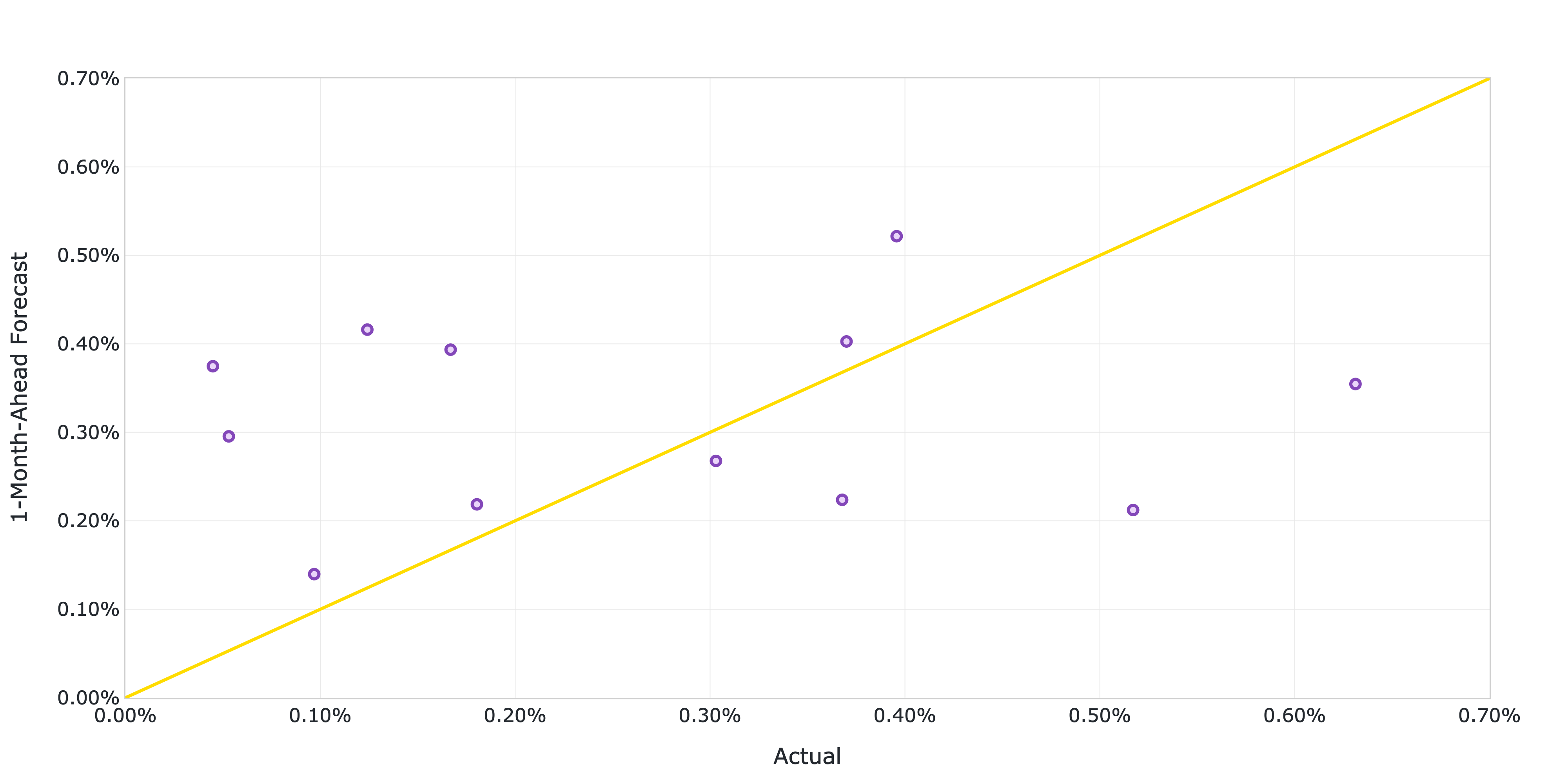

2.4.2 Model quality report

The model quality report includes the model’s performance metrics on the validation data as well as several diagnostic plots, such as actual versus predicted scatter plots and standardized residuals plots. The report shows that the model achieves a root mean squared error (RMSE) of 0.2073%, a mean absolute error (MAE) of 0.1743% and a 60% R-squared on the validation data.

Figure 2: Actual versus predicted US CPI MoM inflation from January 2023 to December 2023.

2.5 Generate the AutoML predictions¶

We now run a batch transform job with the selected pipeline to generate the forecasts over the test set.

# Create the model

model = automl.create_model(

name="us-cpi-model",

sagemaker_session=session,

)

# Create the transformer

transformer = model.transformer(

instance_count=1,

instance_type="ml.m5.xlarge",

)

# Run the transform job

transformer.transform(

data=test_data_s3_uri,

content_type="text/csv",

)

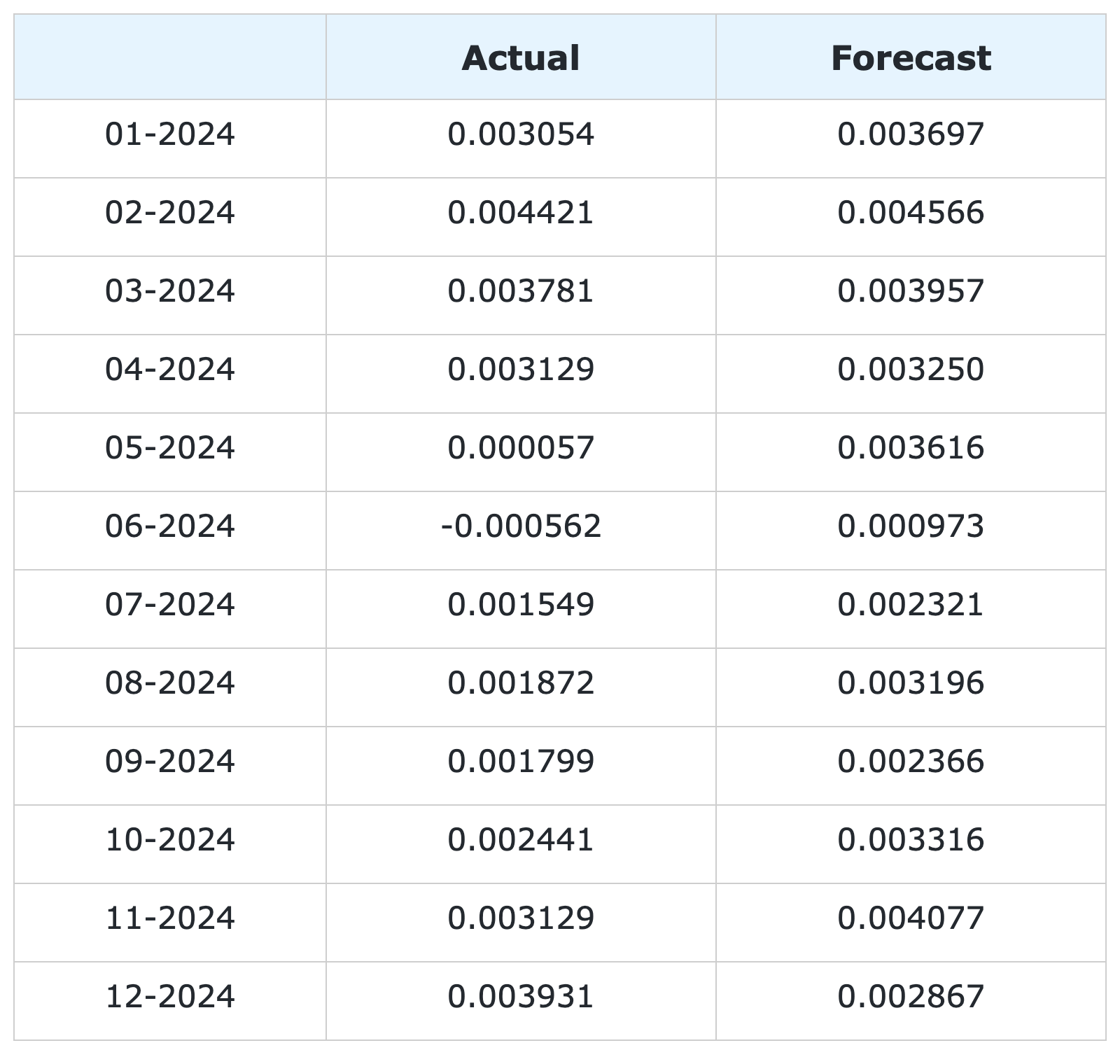

2.6 Evaluate the AutoML prediction¶

After the batch transform job has completed, we can load the forecasts from S3.

# Get the AutoML predictions from S3

predictions = session.read_s3_file(

bucket=bucket,

key_prefix=f"{transformer.latest_transform_job.name}/test.csv.out"

)

# Cast the predictions to data frame

predictions = pd.read_csv(io.StringIO(predictions), header=None)

predictions.index = test_data.index

predictions.columns = ["Forecast"]

# Add the actual values to the data frame

predictions.insert(0, "Actual", test_data[target_name])

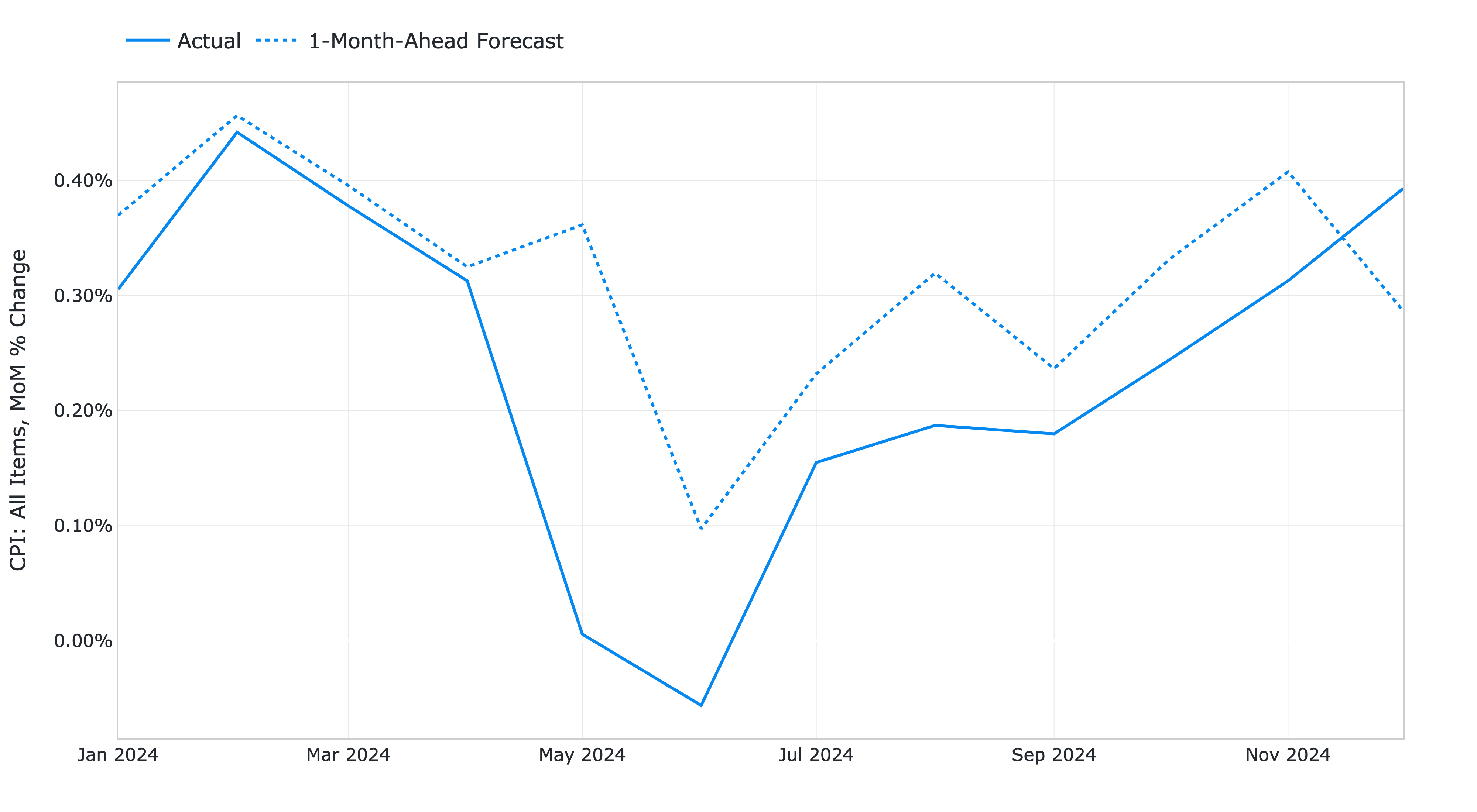

Figure 3: 1-month-ahead AutoML forecasts of US CPI MoM inflation and historical FRED-MD data.

# Calculate the error metrics

errors = pd.DataFrame({

"RMSE": [format(root_mean_squared_error(y_true=predictions["Actual"], y_pred=predictions["Forecast"]), ".4%")],

"MAE": [format(mean_absolute_error(y_true=predictions["Actual"], y_pred=predictions["Forecast"]), ".4%")]

})

# Calculate the correlations between the predictions and the actual values

correlations = predictions.corr()

The RMSE is 0.1322% while the MAE is 0.0978%. The forecasts display a relatively high correlation with the data (78% R-squared), even though some significant deviations are observed on a few months.

Figure 4: 1-month-ahead AutoML forecasts of US CPI MoM inflation against historical FRED-MD data from January 2024 to December 2024.

You can download the Amazon SageMaker notebook with the full code from our GitHub repository.

References¶

[1] Das, P., Ivkin, N., Bansal, T., Rouesnel, L., Gautier, P., Karnin, Z., Dirac, L., Ramakrishnan, L., Perunicic, A., Shcherbatyi, I. and Wu, W., (2020). Amazon SageMaker Autopilot: a white box AutoML solution at scale. In Proceedings of the Fourth International Workshop on Data Management for End-to-End Machine Learning, 1-7. doi: 10.1145/3399579.3399870.

[2] McCracken, M. W., & Ng, S. (2016). FRED-MD: A monthly database for macroeconomic research. Journal of Business & Economic Statistics, 34(4), 574-589. doi: 10.1080/07350015.2015.1086655.

[3] Medeiros, M. C., Vasconcelos, G. F., Veiga, Á., & Zilberman, E. (2021). Forecasting inflation in a data-rich environment: the benefits of machine learning methods. Journal of Business & Economic Statistics, 39(1), 98-119. doi: 10.1080/07350015.2019.1637745.

[4] Hauzenberger, N., Huber, F., & Klieber, K. (2023). Real-time inflation forecasting using non-linear dimension reduction techniques. International Journal of Forecasting, 39(2), 901-921. doi: 10.1016/j.ijforecast.2022.03.002.

[5] Paranhos, L. (2025). Predicting Inflation with Recurrent Neural Networks. International Journal of Forecasting, In press. doi: 10.1016/j.ijforecast.2024.07.010.

Appendix¶

Group 1: Output and Income.

Name |

Description |

|---|---|

CUMFNS |

Capacity Utilization: Manufacturing |

INDPRO |

IP: Index |

IPBUSEQ |

IP: Business Equipment |

IPCONGD |

IP: Consumer Goods |

IPDCONGD |

IP: Durable Consumer Goods |

IPDMAT |

IP: Durable Materials |

IPFINAL |

IP: Final Products (Market Group) |

IPFPNSS |

IP: Final Products and Nonindustrial Supplies |

IPFUELS |

IP: Fuels |

IPMANSICS |

IP: Manufacturing (SIC) |

IPMAT |

IP: Materials |

IPNCONGD |

IP: Nondurable Consumer Goods |

IPNMAT |

IP: Nondurable Materials |

IPB51222S |

IP: Residential Utilities |

RPI |

Real Personal Income |

W875RX1 |

Real personal Income ex Transfer Receipts |

Group 2: Labor Market.

Name |

Description |

|---|---|

USCONS |

All Employees: Construction |

DMANEMP |

All Employees: Durable goods |

USFIRE |

All Employees: Financial Activities |

USGOOD |

All Employees: Goods-Producing Industries |

USGOVT |

All Employees: Government |

MANEMP |

All Employees: Manufacturing |

CES1021000001 |

All Employees: Mining and Logging: Mining |

NDMANEMP |

All Employees: Nondurable goods |

USTRADE |

All Employees: Retail Trade |

SRVPRD |

All Employees: Service-Providing Industries |

PAYEMS |

All Employees: Total nonfarm |

USTPU |

All Employees: Trade, Transportation & Utilities |

USWTRADE |

All Employees: Wholesale Trade |

UEMPMEAN |

Average Duration of Unemployment (Weeks) |

CES2000000008 |

Average Hourly Earnings: Construction |

CES0600000008 |

Average Hourly Earnings: Goods-Producing |

CES3000000008 |

Average Hourly Earnings: Manufacturing |

CES0600000007 |

Average Weekly Hours: Goods-Producing |

AWHMAN |

Average Weekly Hours: Manufacturing |

AWOTMAN |

Average Weekly Overtime Hours: Manufacturing |

CE16OV |

Civilian Employment |

CLF16OV |

Civilian Labor Force |

UNRATE |

Civilian Unemployment Rate |

UEMP15OV |

Civilians Unemployed - 15 Weeks & Over |

UEMPLT5 |

Civilians Unemployed - Less Than 5 Weeks |

UEMP15T26 |

Civilians Unemployed for 15-26 Weeks |

UEMP27OV |

Civilians Unemployed for 27 Weeks and Over |

UEMP5TO14 |

Civilians Unemployed for 5-14 Weeks |

HWI |

Help-Wanted Index for United States |

CLAIMSX |

Initial Claims |

HWIURATIO |

Ratio of Help Wanted/No. Unemployed |

Group 3: Consumption and Orders.

Name |

Description |

|---|---|

HOUSTMW |

Housing Starts, Midwest |

HOUSTNE |

Housing Starts, Northeast |

HOUSTS |

Housing Starts, South |

HOUSTW |

Housing Starts, West |

HOUST |

Housing Starts: Total New Privately Owned |

PERMIT |

New Private Housing Permits (SAAR) |

PERMITMW |

New Private Housing Permits, Midwest (SAAR) |

PERMITNE |

New Private Housing Permits, Northeast (SAAR) |

PERMITS |

New Private Housing Permits, South (SAAR) |

PERMITW |

New Private Housing Permits, West (SAAR) |

Group 4: Orders and Inventories.

Name |

Description |

|---|---|

UMCSENTX |

Consumer Sentiment Index |

ACOGNO |

New Orders for Consumer Goods |

AMDMNOX |

New Orders for Durable Goods |

ANDENOX |

New Orders for Nondefense Capital Goods |

CMRMTSPLX |

Real Manufacturing and Trade Industries Sales |

DPCERA3M086SBEA |

Real Personal Consumption Expenditures |

RETAILX |

Retail and Food Services Sales |

BUSINVX |

Total Business Inventories |

ISRATIOX |

Total Business: Inventories to Sales Ratio |

AMDMUOX |

Unfilled Orders for Durable Goods |

Group 5: Money and Credit

Name |

Description |

|---|---|

BUSLOANS |

Commercial and Industrial Loans |

DTCOLNVHFNM |

Consumer Motor Vehicle Loans Outstanding |

M1SL |

M1 Money Stock |

M2SL |

M2 Money Stock |

BOGMBASE |

Monetary Base |

CONSPI |

Nonrevolving Consumer Credit to Personal Income |

REALLN |

Real Estate Loans at All Commercial Banks |

M2REAL |

Real M2 Money Stock |

NONBORRES |

Reserves Of Depository Institutions |

INVEST |

Securities in Bank Credit at All Commercial Banks |

DTCTHFNM |

Total Consumer Loans and Leases Outstanding |

NONREVSL |

Total Nonrevolving Credit |

TOTRESNS |

Total Reserves of Depository Institutions |

Group 6: Interest Rates and Exchange Rates

Name |

Description |

|---|---|

T1YFFM |

1-Year Treasury C Minus FEDFUNDS |

GS1 |

1-Year Treasury Rate |

T10YFFM |

10-Year Treasury C Minus FEDFUNDS |

GS10 |

10-Year Treasury Rate |

CP3MX |

3-Month AA Financial Commercial Paper Rate |

COMPAPFFX |

3-Month Commercial Paper Minus FEDFUNDS |

TB3MS |

3-Month Treasury Bill |

TB3SMFFM |

3-Month Treasury C Minus FEDFUNDS |

T5YFFM |

5-Year Treasury C Minus FEDFUNDS |

GS5 |

5-Year Treasury Rate |

TB6MS |

6-Month Treasury Bill |

TB6SMFFM |

6-Month Treasury C Minus FEDFUNDS |

EXCAUSX |

Canada / U.S. Foreign Exchange Rate |

FEDFUNDS |

Effective Federal Funds Rate |

EXJPUSX |

Japan / U.S. Foreign Exchange Rate |

BAAFFM |

Moody’s Baa Corporate Bond Minus FEDFUNDS |

AAAFFM |

Moody’s Aaa Corporate Bond Minus FEDFUNDS |

AAA |

Moody’s Seasoned Aaa Corporate Bond Yield |

BAA |

Moody’s Seasoned Baa Corporate Bond Yield |

EXSZUSX |

Switzerland / U.S. Foreign Exchange Rate |

TWEXAFEGSMTHX |

Trade Weighted U.S. Dollar Index |

EXUSUKX |

U.S. / U.K. Foreign Exchange Rate |

Group 7: Prices

Name |

Description |

|---|---|

CPIAUCSL |

CPI: All Items |

CPIULFSL |

CPI: All Items less food |

CUSR0000SA0L5 |

CPI: All items less medical care |

CUSR0000SA0L2 |

CPI: All items less shelter |

CPIAPPSL |

CPI: Apparel |

CUSR0000SAC |

CPI: Commodities |

CUSR0000SAD |

CPI: Durables |

CPIMEDSL |

CPI: Medical Care |

CUSR0000SAS |

CPI: Services |

CPITRNSL |

CPI: Transportation |

OILPRICEX |

Crude Oil, Spliced WTI and Cushing |

WPSID62 |

PPI: Crude Materials |

WPSFD49502 |

PPI: Finished Consumer Goods |

WPSFD49207 |

PPI: Finished Goods |

WPSID61 |

PPI: Intermediate Materials |

PPICMM |

PPI: Metals and metal products |

DDURRG3M086SBEA |

Personal Consumption Expenditures: Durable goods |

DNDGRG3M086SBEA |

Personal Consumption Expenditures: Nondurable goods |

DSERRG3M086SBEA |

Personal Consumption Expenditures: Services |

PCEPI |

Personal Consumption Expenditures: Chain Index |

Group 8: Stock Market

Name |

Description |

|---|---|

S&P 500 |

S&Ps Common Stock Price Index: Composite |

S&P: INDUST |

S&Ps Common Stock Price Index: Industrials |

S&P DIV YIELD |

S&Ps Composite Common Stock: Dividend Yield |

S&P PE RATIO |

S&Ps Composite Common Stock: Price-Earnings Ratio |

VIXCLSX |

VIX |